Freelancing appears to be the new buzzword hailed for its flexibility. Moonlighting employees are under a shadow, as employers share opinions about the acceptability of working for competitors.

It may sound like an oxymoron, but employees tasted freedom during the lockdown. They loved the flexible working arrangements, ability to manage personal responsibilities along with a job and the absence of long commutes and traffic jams.

Many opted for hybrid models, when asked to work from office. The Great Resignation is now seen as a phenomenon, as people quit jobs in unprecedented numbers.

The lay-offs at Byju’s and Twitter will push many more into the freelancer and self-employed space.

FREELANCING VS. MOONLIGHTING VS. SELF-EMPLOYMENT

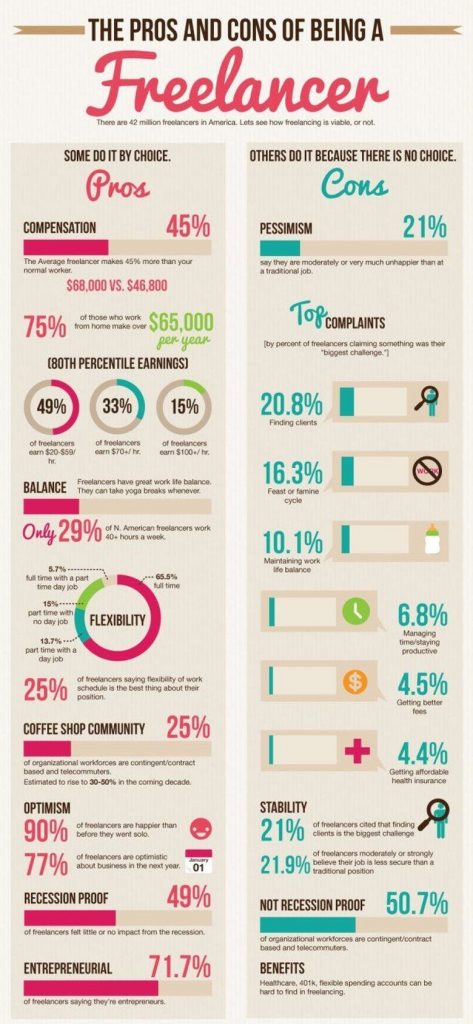

Freelancing is taking up temporary assignments with different employers. Companies seem to favor this model, as it saves cost on paying permanent employee benefits. Hiring someone when needed fits into the just-in-time model.

Moonlighting is a similar assignment for others, while in employment of one company. This has come into fire recently, as double employment is seen as unethical.

Are freelancers self-employed? Yes, but self-employment is doing things with an entrepreneurial streak. It could be a small business or freelancing.

HOW FREELANCING WORKS?

Freelancing looks like a ticket to freedom. It may also pave the way for future employment.

The common factor in the three models is lack of retirement benefits, health insurance, perks and perquisites. One needs to be financially prepared for different situations with no cushion to protect.

One needs self-promotion and brand-building to get work. The simplest option is having a professionally identifiable profile on social media. YouTube and Canva are tools to create and share content. In short, online visibility is non-negotiable. Gone are the days when word-of-mouth helped, though the system is not completely extinct. Testimonials and story-telling (both personal and business) lend credibility.

There may be ‘dry patches’ when there is no income.

FREELANCING TOOLS

- What are the platforms you intend using? This refers to freelancing websites like Freelancer, Upwork, Fiverr or similar ones. There are many others for trainers and coaches which promise to connect the demand and supply side.

- How will you get paid? Do you need to have an account on Paypal, Razorpay, Instamojo, Cashfree or similar payment gateways?

- What is the risk involved? Do you need legal assistance to help with your contracts?

- How will you market your services? Do you need to pay commissions or a fee to those who help you in client acquisition?

- Do you need reskill or upskill yourself with courses or certifications?

5 WAYS TO BE FINANCIALLY PREPARED FOR FREELANCING

1. INVESTMENT

The above questions point to the fact that being self-employed needs an investment. Calculate the cost based on above parameters, and make a provision for it.

Every platform has a free version and a paid version. Make use of free platforms as much as possible. Do your research well. It makes sense to use free platforms in the initial period.

Free online courses on many subjects are available, but they only scrape the surface of the topic. However, knowing the basics saves on money you might pay someone else for content creation or lead generation. If certifications are mandatory for your work, or you need the networking, don’t scrimp on self-development expenses.

At the same time, don’t get carried away by false projections. Check out if work is available in the given field. Coaching, training, image consultancy, counsellor certifications are some examples where companies earn more by selling certifications than doing actual work for clients.

2. EMERGENCY FUND

Ideally, don’t quit your job without creating a financial buffer equivalent to 6-12 months’ expenses.

Calculate monthly expenses on essential costs plus a little extra. You may have to cut down on lifestyle costs (shopping, dining out, entertainment, holidays) for a while. While your home provides wonderful flexible working space, your electricity and internet costs also go up.

In extreme cases, people choose to move to a smaller house or one in the suburbs to save on rent or EMI payments. It needs to be balanced with commuting cost, if you have to work from the client’s premises.

3. HEALTH INSURANCE

Have a fresh look at the health insurance needs of your family. You are no longer covered by employer’s group insurance.

The criticality of family coverage is often overlooked. A friend’s mother needed to undergo a surgery, when she received a new job offer. The new company did not cover parents under their group insurance. They did not agree to an extension of joining date either. She forfeited the offer, because the medical costs involved were high.

Check if your parents are well covered for life and health. It will prevent a drain on your wallet, should an emergency arise.

4. LIFE INSURANCE

I don’t see life insurance for home makers as a subject of women empowerment. It has no direct benefits for the woman concerned.

But do estimate the cost of hiring domestic help, tutors and drivers if the pillar that holds your house together falls. Do buy life insurance for homemakers, be they a wife, mother or mother-in-law.

5. BUDGETING

You need to have an annual budget where you provide for insurance premiums and other annual expenses.

Other than that, you need to make a fresh budget every month, based on estimated cash inflows. Staggered or delayed payments can upset the applecart.

Download the book “7 Money Lessons from the Pandemic” here.